Note: In 2020, I posted an updated assessment of Qliance.

“Healthcare Innovations in Georgia:Two Recommendations”, the report prepared by the Anderson Economic Group and Wilson Partners (AEG/WP) for the Georgia Public Policy Foundation, makes some valuable contributions to deliberations about direct primary care. The AEG/WP team clearly explained their computations and made clear the assumptions underlying their report.

This facilitates the public discussion that the Georgia Public Policy Foundation sought to foster in publishing the report. I have been examining those assumptions in prior posts and there are more to come. In this post, I continue a multi-post evaluation of AEG/WP’s claims regarding the effectiveness of direct primary care in reducing downstream care costs.

Washington State is deservedly recognized as the birthplace and one of the most prominent frontiers for DPC, in large part because of Qliance. The Seattle-based DPC conglomerate is recognized as an exemplary market force in the private sector of health care. Major investors such as Amazon CEO Jeff Bezos have propelled Qliance . . .

Katherine Restrepo and Daniel McCorry, Forbes, February 6, 2017, States Prove Why Direct Primary Care Should Be A Key Component To Any Health Care Reform Plan

Qliance certainly seemed to have muscle. It had 25,000 member patients, revenues approaching $2 million a month, and service contracts with individuals, small and large self-insuring employers, unions, Medicaid, and even on-exchange plans. And it operated in Washington, a state whose regulatory environment has been cited as ideal by advocates favoring direct primary care,

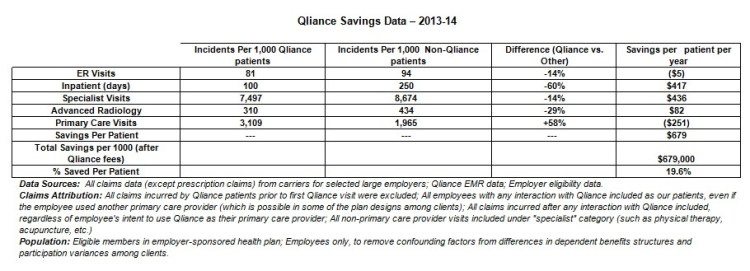

In January 2015, Qliance published some results of a study that claimed that its direct primary care model for employee groups had achieved a 20% overall cost reduction and a net benefit of just under $680 per year for each covered person when compared to those who received traditional, fee-for-service primary care. Qliance monthly fees being in the vicinity of $79 per person per month, those companies, unions, or other health plan partners lucky enough to have Qliance contracts were said, in effect, to have received their money back plus a dividend of at least 70% per annum.

Principles taught in business school will tell you that, provided Qliance could actually demonstrate that these claims were solid and scalable, Qliance would almost certainly have been awash in new health-plan partners and would have had no problem in finding lenders or investors to support its seemingly inevitable growth.

Yet, less than ten days after receiving high praise in Forbes in February 2017, Qliance announced that it was in such deep financial trouble that it was the beneficiary of a GoFundMe campaign. Then, three months later, the marketplace executed its final judgment on Qliance, and the company filed for bankruptcy. The actual business world in which due diligence is practiced appears to have concluded that Qliance could not deliver the value it claimed.

Here, in Qliance’s own table, are the exact promises of immense cost savings that Qliance put before insurers, investors, and lenders:

There is an oddity in first row of data, the one addressing ER visits. Qliance patients are revealed to have fewer, but more expensive, visits than the comparison group. In the aggregate, the fifth column reports, Qliance patients had higher per patient claims costs for emergency room. It seems fair to imagine that Qliance’s apparent admission that it does not reduce ER claims costs may have itself generated skepticism about the claims cost reductions for which Qliance did attempt to take credit.

Qliance’s former president and chief executive office, Erika Bliss, M.D., has expressed outrage that some insurers refused to work with her company even though she told them that Qliance could save them 20% on overall costs.

Qliance’s table points to a per employee per month {“PMPM”) savings of close to $60.

“$40 PMPM is a lot of money for an insurer. When I worked at UPMC Health Plan, [getting a] $40 PMPM from a significant chunk of the covered population would make quite a few VPs very happy as this solves a reasonable chunk of their margin generation expectations.

David Anderson, Research Associate, Duke University, “Points of Confusion“

When insurers walk away from an offer of $55 PMPMs, it is almost certainly because they do not find the offer credible. And in all likelihood their skepticism turned on Qliance’s inability to demonstrate that the Qliance population and the comparison group had similar risk profiles. Risk is the lens through which insurers see, mostly, everything.

Risk is also the lens through which careful research about fixed-fee primary care compensation systems sees the future. Consider, for example, these recommendations of Family Medicine for America’s Health, an alliance of the American Academy of Family Physicians and seven other family medicine leadership organizations, for a prospective payment system for primary care:

Based on our findings, we recommend that a comprehensive primary care payment methodology incorporate the following key components and best practices:

1. Primary Care Payment Rate: The CPCP payment rate should account for approximately 10-12% of total health care costs, in contrast to the roughly 9% supported by high performing health systems today.

2. Population Risk Adjustment: The payment should be risk adjusted using a hybrid model including the Primary Care Activity Level (PCAL) framework with a Minnesota Complexity Assessment Model (MCAM), component. . . .

. . .

FMAH Comprehensive Primary Care Payment Background Report

That FMAH report referred, with emphatic approval, both to Qliance specifically and to direct primary care in general. And the report even relied on none other than Erika Bliss herself to support the idea that patient panels should be divided by risk to assure that the payment reflects adequately the service level required for patients of varying needs; apparently, this is something that Qliance has done in one or more of its programs.

No one from Qliance and none of Qliance’s boosters has even bothered to suggest, let alone present evidence, that the two populations compared in Qliance’s cost reduction analysis had comparable risk profiles. But what was said about possible “selection bias” is far less important than what insurers thought about that possibility. It’s hard to turn one’s back on $60 PMPMs. Things are highly likely to have turned out differently, no matter Qliance said, if insurers were convinced that the purported ability of Qliance and its direct primary care model to reduce overall care costs by 20% was genuine, rather a mere artifact of selection bias.

The table above, produced by Qliance to illustrate its claim of overall costs savings, excludes prescription drug costs. Given that there are prescription drugs which if taken regularly can avert the need for expensive hospital services and given that some prescription drugs can be quite expensive, it is difficult to see how an analysis of overall care cost reductions can exclude prescription drugs.

P.S. It seems at least possible that the “($5)” in the Qliance chart was an erroneous attempt to enter “$5”. Even that, however, seems likely to undermine the credibility of the report — for the same reasons that listing “Bachelor of Arts, Yael University, New Haven” might undermine some other assertions in a resume.]