“Healthcare Innovations in Georgia:Two Recommendations”, the report prepared by the Anderson Economic Group and Wilson Partners (AEG/WP) for the Georgia Public Policy Foundation, makes some valuable contributions to deliberations about direct primary care. The AEG/WP team clearly explained their computations and made clear the assumptions underlying their report.

This facilitates the public discussion that the Georgia Public Policy Foundation sought to foster in publishing the report. I have been examining those assumptions in prior posts and there are more to come. In this post, I continue a multi-post evaluation of AEG/WP’s claims regarding the effectiveness of direct primary care in reducing downstream care costs.

As noted in a prior post, the report by the Anderson Economic Group and Wilson Partners supported the assumption that direct primary care reduces downstream care cost by 15% with nothing more than a cryptic reference to “research and case studies prepared by Wilson Partners”, presented with neither data nor citation. Initially, I thought this secreted research effort might focus on the experience drawn from the SALTA direct care clinics in Michigan.

Let me explain.

David Wilson, the principal of Wilson Partners, co-founded SALTA Direct. At the time of the report, SALTA charged self-insuring self-insuring employers and individual members $70 a month. Wilson’s direct primary care company also boasted that, “The SALTA Direct Primary Care solution has been shown to reduce overall healthcare costs by 20%.”

Wilson’s own company, in other words, both operated at the Qliance-like prices and touted the Qliance-like results needed to support the cost-effectiveness claims assumed by Wilson and his AEG/WP report colleagues. Because of David Wilson’s unique proximity to the SALTA experience, I somehow assumed that data from SALTA formed the backbone of the “research and case studies prepared by Wilson Partners” on which the conclusions of the AEG/WP report so heavily rest.

Well, silly me! The research performed by Wilson Partners for the AEG/WP study apparently did not include any of the cost and performance data of which David Wilson’s SALTA proudly boasts.

Instead, the AEG/WP report authors responded to my request for information by indicating that the “research and case studies prepared by Wilson Partners” comprised the harvesting of three items off the web. One of them was an e-zine article about the CHI clinic. The other two were promotional brochures, denominated as case studies, by the DPC companies Paladina and Nextera and to solicit business from self-insuring employers.

In two upcoming posts, I will examine these items. If they provide sound evidence that direct primary care reduces the costs of downstream care, no one need bother to ask why Wilson’s partnership eschewed data from Wilson’s company.

“Healthcare Innovations in Georgia:Two Recommendations”, the report prepared by the Anderson Economic Group and Wilson Partners (AEG/WP) for the Georgia Public Policy Foundation, makes some valuable contributions to deliberations about direct primary care. The AEG/WP team clearly explained their computations and made clear the assumptions underlying their report.

This facilitates the public discussion that the Georgia Public Policy Foundation sought to foster in publishing the report. I have been examining those assumptions in prior posts and there are more to come. In this post, I continue a multi-post evaluation of AEG/WP’s claims regarding the effectiveness of direct primary care in reducing downstream care costs.

A unique and powerful opportunity for quantitatively informed assessment of such claims has come from a DPC clinic serving employees of Union County. There, health plan members are able to choose between receiving primary care in a DPC clinic or through physicians under traditional model of insurance and fee for service.

Mark Watson is the county official responsible for this innovation. He made available some key data needed for comparing medical costs for DPC patients and those receiving primary care to the John Locke Foundation (“JLF” is NC’s version of GPPF) and others, . The most recent report about Union County by JLF claims that DPC patients experience costs that are 28% lower than those in traditional primary care.

But the very same report expressly notes that the DPC group patients have lower medical risk scores than the traditional group patients.

A large part of medical risk scoring derives from patient age. In that regard, Watson had Union County’s human resources office compile basic demographic data on the two populations. These data showed that the average participant in the DPC group was at the time of compilation about four years younger than an average participant counterpart in the traditional group.

Four years may not seem like much, but age/claim cost curves are steep. A figure of 5:1 is widely cited in comparing the medical claims experience of 64 year-olds relative to 21 year-olds. Even an age/cost curve with an average slope of 4:1 can explain every penny of the 28% cost differential between two Union County groups separated in age by four years. If the 5:1 ratio most broadly accepted is accurate, than Union County’s primary care option actually increased the county’s costs.

It is virtually certain that what looks like a claims cost reduction is an illusion resulting from the segmentation of Union County’s insureds by selection bias.

Likely sources of selection bias at the Union County clinic are discussed here.

Union County’s presentation of comparative claims data is available here.

Union County’s summary of comparative age data is available here.

Union County’s contract with its direct primary care clinic operator is available here.

Update: See this post for some cost-adjusted data that confirms signficant selection bias, while still suggesting that direct primary care has net positive effects.

“Healthcare Innovations in Georgia:Two Recommendations”, the report prepared by the Anderson Economic Group and Wilson Partners (AEG/WP) for the Georgia Public Policy Foundation, makes some valuable contributions to deliberations about direct primary care. The AEG/WP team clearly explained their computations and made clear the assumptions underlying their report.

This facilitates the public discussion that the Georgia Public Policy Foundation sought to foster in publishing the report. I have been examining those assumptions in prior posts and there are more to come. In this post, I continue a multi-post evaluation of AEG/WP’s claims regarding the effectiveness of direct primary care in reducing downstream care costs.

Washington State is deservedly recognized as the birthplace and one of the most prominent frontiers for DPC, in large part because of Qliance. The Seattle-based DPC conglomerate is recognized as an exemplary market force in the private sector of health care. Major investors such as Amazon CEO Jeff Bezos have propelled Qliance . . .

Katherine Restrepo and Daniel McCorry, Forbes, February 6, 2017, States Prove Why Direct Primary Care Should Be A Key Component To Any Health Care Reform Plan

Qliance certainly seemed to have muscle. It had 25,000 member patients, revenues approaching $2 million a month, and service contracts with individuals, small and large self-insuring employers, unions, Medicaid, and even on-exchange plans. And it operated in Washington, a state whose regulatory environment has been cited as ideal by advocates favoring direct primary care,

In January 2015, Qliance published some results of a study that claimed that its direct primary care model for employee groups had achieved a 20% overall cost reduction and a net benefit of just under $680 per year for each covered person when compared to those who received traditional, fee-for-service primary care. Qliance monthly fees being in the vicinity of $79 per person per month, those companies, unions, or other health plan partners lucky enough to have Qliance contracts were said, in effect, to have received their money back plus a dividend of at least 70% per annum.

Principles taught in business school will tell you that, provided Qliance could actually demonstrate that these claims were solid and scalable, Qliance would almost certainly have been awash in new health-plan partners and would have had no problem in finding lenders or investors to support its seemingly inevitable growth.

Yet, less than ten days after receiving high praise in Forbes in February 2017, Qliance announced that it was in such deep financial trouble that it was the beneficiary of a GoFundMe campaign. Then, three months later, the marketplace executed its final judgment on Qliance, and the company filed for bankruptcy. The actual business world in which due diligence is practiced appears to have concluded that Qliance could not deliver the value it claimed.

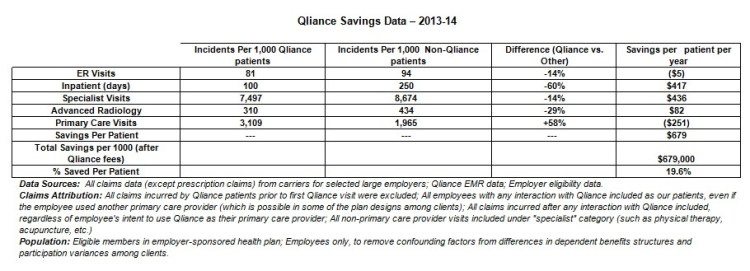

Here, in Qliance’s own table, are the exact promises of immense cost savings that Qliance put before insurers, investors, and lenders:

There is an oddity in first row of data, the one addressing ER visits. Qliance patients are revealed to have fewer, but more expensive, visits than the comparison group. In the aggregate, the fifth column reports, Qliance patients had higher per patient claims costs for emergency room. It seems fair to imagine that Qliance’s apparent admission that it does not reduce ER claims costs may have itself generated skepticism about the claims cost reductions for which Qliance did attempt to take credit.

Qliance’s former president and chief executive office, Erika Bliss, M.D., has expressed outrage that some insurers refused to work with her company even though she told them that Qliance could save them 20% on overall costs.

Qliance’s table points to a per employee per month {“PMPM”) savings of close to $60.

“$40 PMPM is a lot of money for an insurer. When I worked at UPMC Health Plan, [getting a] $40 PMPM from a significant chunk of the covered population would make quite a few VPs very happy as this solves a reasonable chunk of their margin generation expectations.

When insurers walk away from an offer of $55 PMPMs, it is almost certainly because they do not find the offer credible. And in all likelihood their skepticism turned on Qliance’s inability to demonstrate that the Qliance population and the comparison group had similar risk profiles. Risk is the lens through which insurers see, mostly, everything.

Risk is also the lens through which careful research about fixed-fee primary care compensation systems sees the future. Consider, for example, these recommendations of Family Medicine for America’s Health, an alliance of the American Academy of Family Physicians and seven other family medicine leadership organizations, for a prospective payment system for primary care:

Based on our findings, we recommend that a comprehensive primary care payment methodology incorporate the following key components and best practices:

1. Primary Care Payment Rate: The CPCP payment rate should account for approximately 10-12% of total health care costs, in contrast to the roughly 9% supported by high performing health systems today.

2. Population Risk Adjustment: The payment should be risk adjusted using a hybrid model including the Primary Care Activity Level (PCAL) framework with a Minnesota Complexity Assessment Model (MCAM), component. . . .

. . .

FMAH Comprehensive Primary Care Payment Background Report

That FMAH report referred, with emphatic approval, both to Qliance specifically and to direct primary care in general. And the report even relied on none other than Erika Bliss herself to support the idea that patient panels should be divided by risk to assure that the payment reflects adequately the service level required for patients of varying needs; apparently, this is something that Qliance has done in one or more of its programs.

No one from Qliance and none of Qliance’s boosters has even bothered to suggest, let alone present evidence, that the two populations compared in Qliance’s cost reduction analysis had comparable risk profiles. But what was said about possible “selection bias” is far less important than what insurers thought about that possibility. It’s hard to turn one’s back on $60 PMPMs. Things are highly likely to have turned out differently, no matter Qliance said, if insurers were convinced that the purported ability of Qliance and its direct primary care model to reduce overall care costs by 20% was genuine, rather a mere artifact of selection bias.

The table above, produced by Qliance to illustrate its claim of overall costs savings, excludes prescription drug costs. Given that there are prescription drugs which if taken regularly can avert the need for expensive hospital services and given that some prescription drugs can be quite expensive, it is difficult to see how an analysis of overall care cost reductions can exclude prescription drugs.

P.S. It seems at least possible that the “($5)” in the Qliance chart was an erroneous attempt to enter “$5”. Even that, however, seems likely to undermine the credibility of the report — for the same reasons that listing “Bachelor of Arts, Yael University, New Haven” might undermine some other assertions in a resume.]

“Healthcare Innovations in Georgia:Two Recommendations”, the report prepared by the Anderson Economic Group and Wilson Partners (AEG/WP) for the Georgia Public Policy Foundation, makes some valuable contributions to deliberations about direct primary care. The AEG/WP team clearly explained their computations and made clear the assumptions underlying their report.

This facilitates the public discussion that the Georgia Public Policy Foundation sought to foster in publishing the report. I have been examining those assumptions in prior posts and there are more to come. In this post, I begin a multi-post evaluation of AEG/WP’s claims regarding the effectiveness of direct primary care in reducing downstream care costs.

The focal assumption of the AEG/WP report’s calculations is that DPC membership will reduce the claims cost for downstream care by 15%, a number represented as a low end estimate. The sole support offered in the AEG/WP report for this 15% presumption is a statement that, “the factor is based on research and case studies prepared by Wilson Partners”. The report gives no description of the research or case studies that Wilson Partners prepared; no methodology is identified; the subjects of the case studies are not identified; the report presents no research data; and the report has no citations of, or reference to, any public source where any support of any kind for the 15% factor, or any similar factor, can be found.

The AEG/WP report does present more than four hundred data points in six tables that predict that billion dollar savings are possible, if AEG/WP’s key assumptions about direct primary care are correct.The number of data points presented in the 75 page AEG/WP report that address whether direct primary care has any gross or net cost-reduction value is precisely zero.

Of the billion dollar savings AEG/WP predicts, not a penny would be realized unless the question of whether direct primary care significantly reduces the claim costs of downstream care is answered in the affirmative.

That’s the real billion dollar question, to which AEG/WP’s apparent answer is, “Trust us, we did some studies.”

When an opinion piece in JAMA suggested that direct primary care might resemble primary care capitation plans sometimes tried by insurers in raising issues of allocating resources between primary care and other medical care, Kenneth Qiu, M.D. gathered enthusiastic approval from many supporters of direct primary for the following response.

DPC looks like capitation but is not. Capitation incentivizes less visits and more referrals while DPC does the opposite. To illustrate the difference in underlying psychology and motivation between DPC and capitation, imagine I make and sell lemonade. If I set a price for the lemonade and a customer pays for my lemonade, I’m going to ensure the customer gets the best lemonade possible and will do everything in my power to ensure quality so the customer keeps coming back. This is DPC. Now, if a big company puts me in a network of lemonade sellers and says they will pay me a certain amount per customer and will assure customers come by putting my name on the in-network list, I’m likely going to create a watered down product that just barely counts as lemonade in order to maximize my payment from the big company since customers are coming anyways and, at the end of the day, its the company that pays me, not the customer. This is capitation. As it relates to primary care, better lemonade means more access and better, more comprehensive treatment, both medical and personal.

I’ve sold lemonade on the streets, and I don’t get it.

Of course I made the best possible lemonade to keep my “fee-for-cup” drinkers coming back, as well as to gain new “fee-for cup” drinkers from referrals. But I don’t see why my lemonade would be any different if those fee-for-cup payments came from the Lemonade Club (LC) rather than from drinkers directly. I will be under pressure to perfect the mix of lemonade quality, lemonade dilution, and lemonade production costs that will keep my drinkers satisfied and myself in business, no matter who makes the payments.

Suppose, however, LC puts me on a capitation system that parallels primary care capitation by insurers, and continued participation requires that I provide all-you-can-drink lemonade. The quality, dilution, and production cost mix may need adjustment. I may well have to make a more dilute lemonade to make the business work. But, while the Lemonade Club can perhaps lead a drinker toward this potentially watered-down lemonade (by putting you on its “Lemonade Near You” app), it can’t make him drink and it can’t make him remain on my panel of drinkers. Because I’ll still need drinkers walking up to the stand, I will continue to make the best lemonade possible given the restraints of all-you-can-drink, fixed-fee lemonade.

Dr Qiu is simply wrong to assume that lemonade customers would keep coming simply because I am on the Lemonade Club list. By the very defintion of list, there are actually other lemonade makers on the same LC list.

How are things different for the lemonade entrepreneur outside the LC network who decides for herself to seek customers for a fixed-fee all-you-can-drink plan that parallels direct primary care?

Yes, she may not like working with “Big Lemonade” in general, or Lemonade Club in particular. But another lemonader might like being on an app that finds “nearest lemonade”. Yes, she might not like spending the time filling out LC paperwork; but maybe it would take another lemonader less effort to work out a single contract with LC than it does to negotiate price and credit terms with individual drinkers.

And consider this, if Dr Qiu has opened his own Direct Lemonade stand, and has a panel that have prepaid a season’s worth of lemonade in advance, his incentive to keep his quality up all season long might be only a little bit different from his Lemonade Club branded competitor.

Note, too, that Dr Qiu – like his competitior – might be at risk of adverse selection by those heavy drinkers who are disproportionately attracted to all-you can-drink fixed-fee lemonade. Who would blame him if he targeted connaisseurs de limonade who sipped rather than gulped?

Yes, direct primary care has virtues. But, it in terms of incentivizing fewer visits and more referrals, or an alternative strategy of cherry-picking low-utilizers, a lemonading practice that turns on a fixed-fee for potentially unlimited visits resembles capitation in several important ways.

A billion here, a billion there, and pretty soon you’re talking real money.

Attributed to Senate Everett Dirkson (R-IL, deceased)

This spreadsheet recomputes net five year savings from direct primary care if AEG/WP’s assumptions of (a) a $70 per month DPC fee that (b) stays constant for the next ten years are replaced with the assumptions of (a) $101 per month DPC for the year 2020 that (b) trends upward at the same rate as other medical costs.

The case for replacing the $70 fee with a $101 fee is set out in this prior post.

The case for replacing the assumption that DPC fees will stay flat for a decade with the assumption that fees will trend upward at the same rate as other medical costs is set out in this prior post.

The same spreadsheet also includes calculators used to determine the expected annual per policy premium savings given different values for the monthly fixed direct primary care fee. The spreadsheet replicates AEG/WP’s computation methodology with precision; cell formulae are readily viewed.

These computations show how the proposed adjustments reduce the computed savings from direct primary care by over 85% from nearly $1.1 billion dollars claimed by AEG/WP reports authors to less than $140 million dollars.

Importantly, the calculations discussed here actually assume the validity of AEG/WP’s major assumption about the ability of direct primary care to reduce the cost of claims for downstream care. This post only addresses the inflation of claimed savings that result from the AEG/WP’s authors being unrealistic about the cost of direct primary care.

Whether these authors were accurate about the effectiveness of direct primary care in reducing claims costs for downstream services is left for other posts. If DPC is as effective as the AEG/WP report assumes, then every direct primary care at realistic prices might still offer $140,000,000 in savings. On the other hand, if direct primary care is only two-thirds as effective as AEG/AP claims, then not a penny of savings would materialize.

In “Healthcare Innovations in Georgia:Two Recommendations”, the report it prepared for the Georgia Public Policy Foundation, the Anderson Economic Group and Wilson Partners (AEG/WP) for the Georgia Public Policy Foundation, clearly explained their computations and made clear the assumptions underlying their report. This facilitates the public discussion that the Georgia Public Policy Foundation sought to foster in publishing the report. I have addressed various aspects of their explanation and assumption in previous blog entries, and more are on the way. Right now I wish to address AEG/WP’s inclusion of a “wellness” program in its direct primary care proposal.

AEG/WP recommended that each large insurer provide a “wellness-demand management program” to each participant who elected direct primary care. This type of voluntary program “uses the results of health risk assessments and claims data to determine a personalized health and well-being curriculum that “would include education, health coaching support, and activity goal-setting and tracking.” It also envisioned “a reward vehicle in the form of a Health Reimbursement Arrangement for members enrolled through employer or group coverage, or a Georgia Healthcare Premium Account for members enrolled through individual coverage” and even a “modest cash incentive could be substituted to encourage particularly reluctant individuals to enter into a wellness plan”.

Naturally, AEG/WP included the positive effects of their wellness plan in computing cost savings from their direct primary care plan. Their estimates of low but gradually growing wellness plan participation and its benefits in improved health in the following years resulted in a set of claims cost reductions that amounted to about 0.5 per cent of claims costs in the second year, 1.0 per cent in the third year, 1.50 percent in the fourth year, and so on. Their computation assumes that by year five over 60,000 members will be enrolled in the wellness program and claim cost reductions would reach 2%.

It is important to note these more modest numbers were then added to the predicted 15% reduction of downstream care costs attributed to direct primary care. So, that in the fifth year, for example, AEG/WP savings computation reflects 17% lower claims costs for DPC participants, but 2% of the 17% is due to the wellness program.

What is concerning is that, while the additional 2% savings in year five is scored as a computed as a positive effect of the AEG/WP direct primary care plan, AEG/WP failed to include in their computation any costs associated with a 60,000 person wellness program; there’s not a penny for the study of the personal claims data, the personalized curricula, the coaching, the rewards. They credited their program with the financial benefits from a wellness program, but did not bother to debit it with the financial costs of a wellness program.

It may be a relatively small amount of money as these things go, about four million dollars in year five. But this instance of inclusion of benefits and the exclusion of their costs seems similar to other, more financially consequential failures of analysis addressed in my other recent posts; one in which the AEG/WP team also looked at one group of DPC practices to determine what the benefits of paying monthly DPC fees are and then at a different group to determine the cost of DPC fees; and another in which the same team determined that downstream cost savings will rise exponentially with rising medical care costs, but assumed that the monthly fees of DPC practices would remain flat.

The Medicaid goal of the political right in Georgia has always been careful stewardship of tax-payer funds. Three years ago, the Georgia Public Policy Foundation began to flog a bargain basement Medicaid waiver plan priced at $2500 per capita.

The core rationale for this seemingly meager amount was that $60-$70 a month direct primary care makes almost all other care unnecessary except in rare “true catastrophic” cases.

Everything from the political right claiming vast advantages for direct primary care needs to be seen in connection with Medicaid cost control efforts.

At the same time, direct primary care advocacy from the right, at least in Georgia right now, also needs to be viewed as intended to support Section 1332 waiver authority for an ACA-market-segmenting limited benefit plan built around direct primary care.

Healthcare Innovations in Georgia: Two Recommendations, the report prepared for the Georgia Public Policy Foundation by the Anderson Economic Group and Wilson Partners, praised the cost-savings benefits of direct primary care. Ostensibly, it did so in support of requiring large insurers to offer direct primary care as a primary care option within comprehensive, full benefit, ACA compliant plans. But the Georgia Public Foundation has ordinarily advocated for direct primary care in a context limited to either (a) controlling public cost for Medicaid and state employee coverage, or (b) opposing the Affordable Care Act itself. The Foundation has, as well, been generally antagonistic toward ACA full benefit plans.

Accordingly, I am not persuaded that GPPF was ever seriously in favor of, or even interested in, expanding choice within the ACA by including direct primary care within full benefit plans. There even appear to be signs within the AEG/WP report itself that earlier drafts may have included specific recommendations for channeling Medicaid and state employees into direct primary care plans with limited benefits.

In any case, there is no sign that the State is moving toward direct primary care within ACA compliant full benefit plans. Instead, with enthusiastic support from GPPF, the State is seeking a waiver to allow and support limited benefit plans. And this enables the AEG/WP to be offered for what I believe more realistically reflects the reasons for which the Georgia Public Policy Foundation commissioned it.

Specifically, in the advocacy from the political right yet to come, I am quite certain the AEG/WP report will be represented as a massive, quantitative study that confirms the cost-effectiveness of direct primary care. Yet, despite its many tables of numbers, its imposing appearance, and its astonishing 75 pages, there is good reason to question whether the AEG/WP report demonstrates that direct primary care has billion dollar value or any value at. Blog posts just prior to this one and a number of subsequent posts address these questions.

Ironically, the best way to test the cost-effectiveness of direct primary care might very well be to create options within comprehensive, full benefit, ACA compliant plans where direct primary care can compete on an even basis in an actual market directly with traditional fee for service primary care. So, kudos to the Georgia Public Policy Foundation for commissioning and publishing the AEG/WP report that presented that idea. Actually getting behind that market-based idea would be even better, and might actually help Georgia blaze a trail for the nation.

That alone makes the AEG/WP report off by about $500,000,000.

In “Healthcare Innovations in Georgia:Two Recommendations”, the report prepared by the Anderson Economic Group and Wilson Partners (AEG/WP) for the Georgia Public Policy Foundation, the authors clearly explained their computations and made clear the assumptions underlying their report. One of the assumptions was that the fixed monthly fee for direct primary care would be $70 a month. I examined that assumption here, and I firmly believe $70 underestimates the fixed monthly fee that would actually be for direct primary care that is actually cost-effective at reducing the costs of downstream care. For this post, however, I will assume that the monthly fee is correctly priced at $70 a month.

In its computation purporting to show a billion dollar savings over the next five years from implementation of direct primary care with more to come in the five years after that, however, AEG/WP made the additional assumption that the $70 monthly fee would remain flat for a decade. That assumption accounts for hundreds of thousands of dollars of the computed savings.

AMG/WP have offered no justification for that assumption. It is hard to imagine how that assumption could possibly be justified. It is even hard to image how a responsible analyst could make such an assumption.

The report reasonably suggests that as medical claim costs rise in compound fashion (by as much as 9.9% per year in the individual market), the amount that might be saved by DPC-attributable cost reductions would also in compound fashion. These potential savings are accounted for in AEG/WP’s computations. Also, an identical upward, and compounding, trend is built in to their computations for the claims costs of traditional primary care.

The AWG/WP report assumes, however, the cost of a DPC membership will hold steady at $70 for an entire decade. Accordingly, in AEG/WP’s computations the medical claim savings from DPC grow exponentially, the costs of traditional primary care grow exponentially, the medical costs of downstream (non-priamry) care services grow exponential but the costs of DPC remain perfectly flat.

Since direct primary care clinics must recruit staff, rent space, and buy goods in the same marketplace as other medical providers, including traditional primary care providers, AEG/WP’s choice to assume a stable $70 clinic fee is problematic.

If the $70 monthly fee is trended up for a decade by the same 9.9% per year AGE/WP selected for its calculation of all other future medical prices, including the cost of traditional primary care, the monthly fee reaches $180 a month, and the annual fee increases by more than $1200. Had AEG/WP chosen to perform their DPC savings computation to reflect such seemingly predictable increases, the computed savings would been lowered by hundreds of thousands of dollars.

Interestingly, the AEG/WP report was published in May 2019. At the time, $70 was exactly the monthly DPC fee being charged by SALTA, a direct primary care company co-founded by David Wilson, one of the AEG/WP authors. By December 2019, however, SALTA announced that its fixed monthly fee was going up by almost 29%, to $90 a month.

Apparently DPC practices are not immune to medical cost inflation — at least if you own one.

Note: This Link will access the Google spreadsheet I used to calculate the effect on premiums of different values for the monthly fixed fee; it follows AEG/WP methodology. It also explores the difference in the individual market for 2025 between assuming that the $70 fee remains flat and assuming that it trends upward in parallel to rate used by AEG/WP to compute all other health care costs.

On that score alone, the AEG/WP report is off by $750,000,000.

In “Healthcare Innovations in Georgia:Two Recommendations”, the report prepared by the Anderson Economic Group and Wilson Partners (AEG/WP) for the Georgia Public Policy Foundation, the authors clearly explained their computations and made clear the assumptions underlying their report. One of the assumptions was that the fixed monthly fee for direct primary care would be $70 a month.

The report itself did not identify the source of the $70 figure. AEG/WP responded by email to an inquiry by stating only that the number was based on a study by Wilson Partners, apparently unpublished, of 16 direct primary care practices.

The experience of now-bankrupt Qliance, discussed elsewhere, further suggests that $70 fees cannot sustain a direct primary care experience that delivers effective cost reduction.

Why did AEG/WP ignore an academic study on point?

But why rely on a tiny unpublished study, when there is a published quantitative study of far greater scope in The Journal of the American Board of Family Medicine, with data directly on point, and a complete description of the methodology used. And might such a study be given special attention when the lead author of that academic journal article is one of the leaders of the direct primary care movement — Dr. Philip Eskew, a member of the advisory board of the Direct Primary Care Alliance and its general counsel.

In their piece prepared in 2014, Direct Primary Care: Practice Distribution and Cost Across the Nation, Dr. Eskew and his colleague reported that 116 practices they had identified as direct primary care practices had an average monthly cost of $93.26

Did AEG/WP ignore Georgia’s largest DPC group?

HIPnation has 40 direct primary care doctors in Georgia, one of seven states in which it operates. HIPnation would likely be a principal beneficiary if the AEG/WP recommendation were implemented. Dr. Hal Scherz, one of HIPnation’s founders, has deeply involved in Georgia Public Policy Foundation advocacy on health care in general and direct primary care in particular. In fact, Scherz’s advocacy is all but certainly part of the story of how AEG/WP came to prepare a report about direct primary care for GPPF.

Dr Scherz’s HIPnation has monthly fixed direct primary care fee of $100 a month. If a monthly fixed fee of $100 is substituted for $70 in AEG/WP’s computation, over half of the calculated savings for the individual market evaporates, along with every penny of savings in the large group and small group markets.

The monthly fees at direct primary care clinics that the Georgia Public Policy Foundation has featured in its own commentary can run $125 or more.

Unlike those Qliance, the doors are still open at the Union County employees’ direct practice clinic, an operation lauded by the Georgia Public Policy Foundation in a copyrighted article. The monthly fee paid by Union County for an employee who elects the DPC clinic run for the county by Paladina Health Services is $125. If a monthly fixed fee of $125 had been used in the calculations of the AEP/WP there would have been no net savings to report in the individual, small group, or large group markets.

In another copyrighted article, then-GPPF-president Kelley McCutcheon praised the PHS/Encounter3 direct primary care clinic in Altoona, Pennsylvania. That clinic offered free or discounted plans to persons with limited incomes. For an enrolled individual with incomes at the national median, however, the monthly fixed direct primary care fee was $130.

$150?

Consider, too, the DPC industry’s reaction to provisions addressing direct primary care in the Primary Care Enhancement Act of 2019, HR3708. That legislation would allow DPC fixed fees up to $150 a month (indexed for inflation) to become countable expenses under Health Savings Accounts. The Direct Primary Care Alliance’s Board of Directors opposes that $150 limitation.

Why did AEG/WP draw its assumption about monthly fees from a different set of clinics than those from which it drew its assumption about effective performance?

To assess what fixed monthly charge actually makes sense, we should look at a few examples of direct primary care clinics that at least claim to have demonstrated their cost-effectiveness. Critique of such claims by AEG/WP and others, I leave for another post. For the moment, though, let us take AEG/WP’s claims of cost-effectiveness at face value.

While AEG/WP did not identify, in the report, the research and case studies on which based their assumptions, AEG/WP responded to an email seeking more information by identifying three clinics as sources for its cost-effectiveness conclusion. It seems abundantly reasonable to assign special significance to the monthly fixed fees at these same institutions in assessing the reasonableness of the $70 fixed fee. The sauce for the cost-effectiveness assumption goose is sauce for the fee assumption gander.

For two of the three AEG/AP hand-selected clinics, the basic monthly fixed fee can be determined from public sources. Nebraska’s CHI Health Centers’ basic charge is $80. The monthly fixed fee at Colorado’s Nextera clinics are $99; since, however, Nextera clinics also charge a $79 one-time registration fee the effective monthly costs at Nextera exceed $99. AEG/WP’s other choice was a clinic operated by Paladina Health Care, who specialize in employer sponsored plans and who do not quote prices to the public. As noted above, however, Paladina is known to receive $125 a month for each adult enrollee in its Union County employee program.

Averaging the monthly fixed fees of CHI, Nextera, and Paladina — the very clinics AEG/WP rely on for their claims of cost-effectiveness — suggests a monthly fixed fee of $101 a month. Note that this number in early 2020 seems very much in line with Dr. Eskew’s 2014 finding of $93 adjusted by low inflation. If $101 is substituted for $70 in AEG/WP’s computation, over half of the calculated savings for the individual market evaporates, along with every penny of savings in the large group and small group markets. Five-year computed savings across all markets would be less than a quarter of the billion dollars claimed by AEG/WP..

Note: This Link will access the Google spreadsheet I used to calculate the effect on premiums of different values for the monthly fixed fee; it follows AEG/WP methodology.